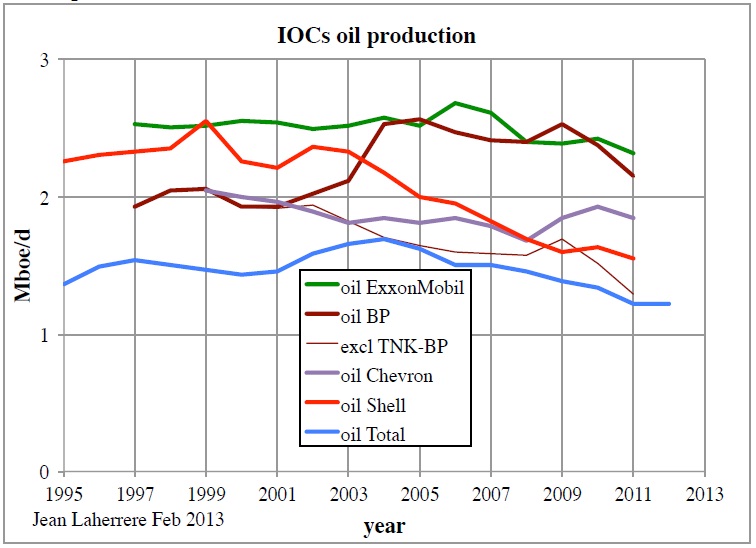

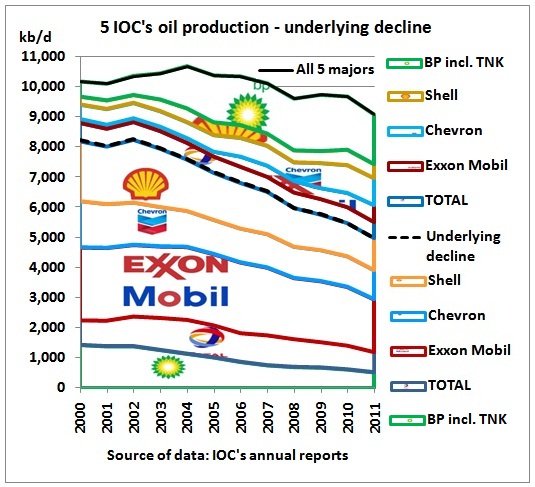

International

oil companies’ oil production peaked in 2004 and declined by 2.1 %

pa

The

peak in

The

peak in

The company began an extensive restructuring after the April 2010 explosion on the Deepwater Horizon rig in the Gulf of Mexico that killed 11 people and unleashed a huge oil spill. Among the asset sales announced, BP agreed Oct. 22 to sell its 50 percent stake in a Russian joint venture, TNK-BP, to the state-controlled Rosneft for about $27 billion in cash and stock.

]

]

Jean’s

production curve includes gas which has been converted to barrels of

oil equivalent.

Jean’s

production curve includes gas which has been converted to barrels of

oil equivalent.

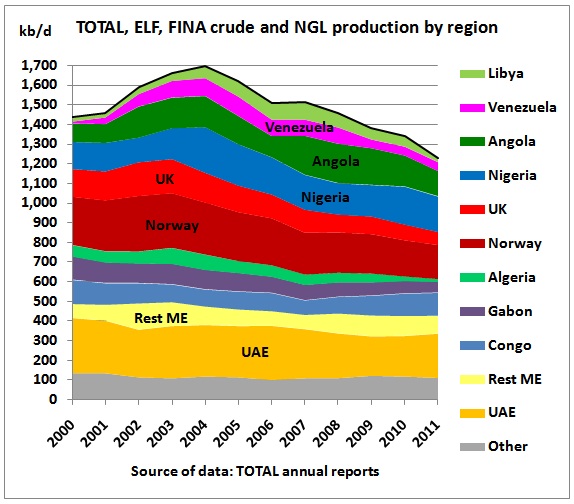

Total’s

oil production peaked in 2004 and declined since then by 4% pa. The

underlying decline rate (declining areas) was also a steep 5.7 % pa.

Total’s

oil production peaked in 2004 and declined since then by 4% pa. The

underlying decline rate (declining areas) was also a steep 5.7 % pa.

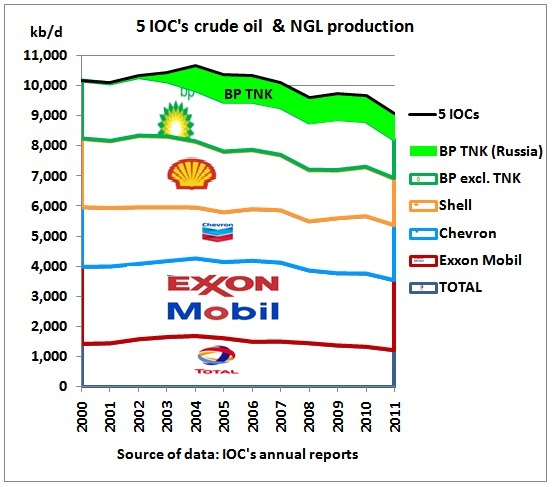

Oil production (crude and NGLs) of 5 international oil companies has been declining by a total of 15% over the period 2004-2011.

11 March, 2013

Merci,

Jean (Lahererre, ASPO France) pour m’avoir envoyé quelques graphes

sur le déclin du production des compagnies pétrolières

internationales. Ça m’a donné l’ideee de faire d’autres

graphes plus détaillés.

We stack the above curves and find a decline rate of 2.1 % between a

peak in 2004 and 2011.

The

peak in

The

peak in

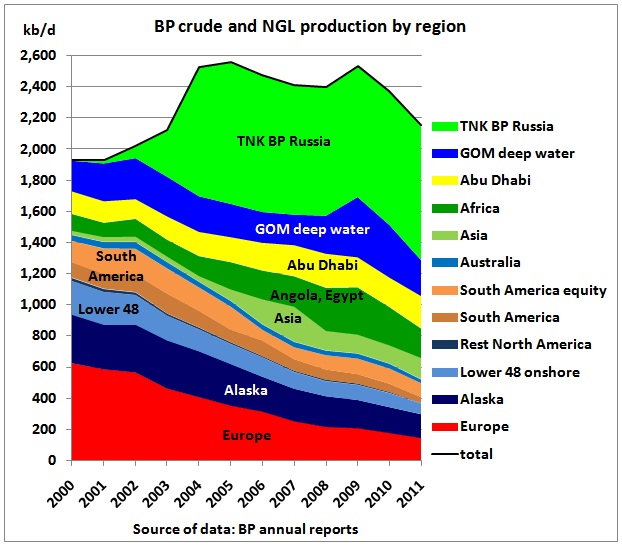

2004 was created by BP acquiring 50% of the Russian oil

assets of Tymen Oil Company (TNK), Onako and Sidanco in 2003. This

asset is being sold again, to pay for damages of the Deepwater

Horizon oil spill.

BP

Earnings Fall on Lower Production and Higher Costs

5/2/2013

5/2/2013

The company began an extensive restructuring after the April 2010 explosion on the Deepwater Horizon rig in the Gulf of Mexico that killed 11 people and unleashed a huge oil spill. Among the asset sales announced, BP agreed Oct. 22 to sell its 50 percent stake in a Russian joint venture, TNK-BP, to the state-controlled Rosneft for about $27 billion in cash and stock.

EU

Commission Clears Acquisition of TNK-BP by

Rosneft

8/3/2013

8/3/2013

Without

BP-TNK, the peak of all 5 IOCs was in 1999 and the over-all decline

rate since then 1.9 % pa

So

let’s have a look at BP first:

]

]

BP's overall decline rate between 2000 and 2011 without BP-TNK was 3% pa.

The underlying decline rate of the declining group (Europe, Alaska,

US lower 48, South America and Australia) was a whopping 5.8 %.

So

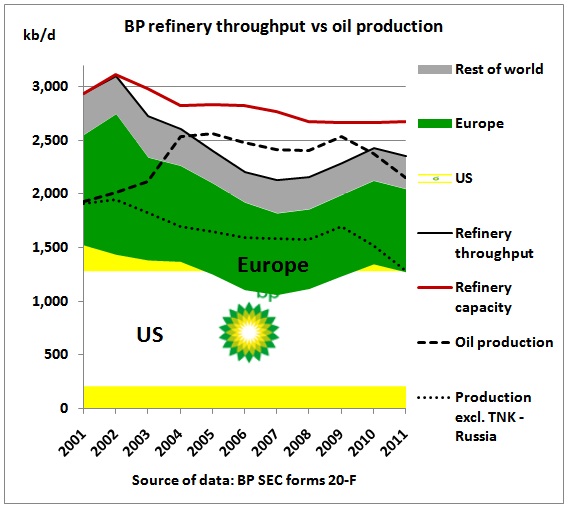

will BP now produce enough oil for their refineries?

This graph shows a comparison of BP’s oil production with the capacity

and throughput of BP’s refineries. The sale of BP-TNK means that,

on a net-basis, BP needs to buy expensive crude oil and other

feedstock on the global market in order to keep their refineries

going.

All

data for the above graphs can be found here (BP annual reports):

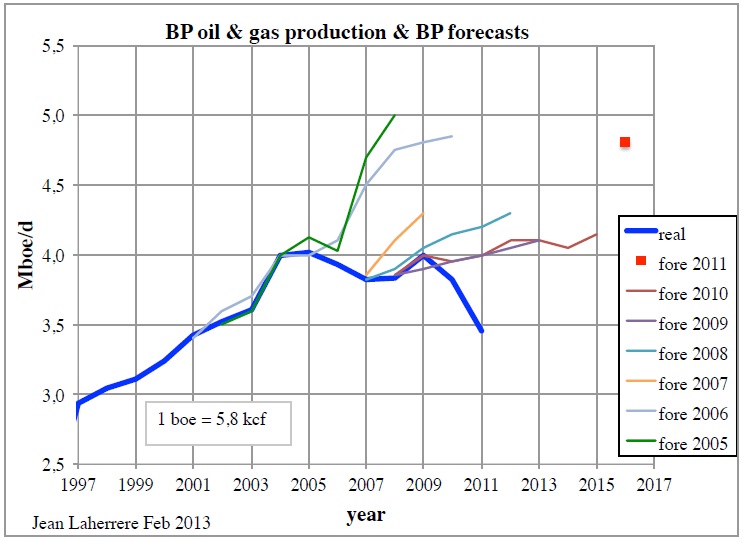

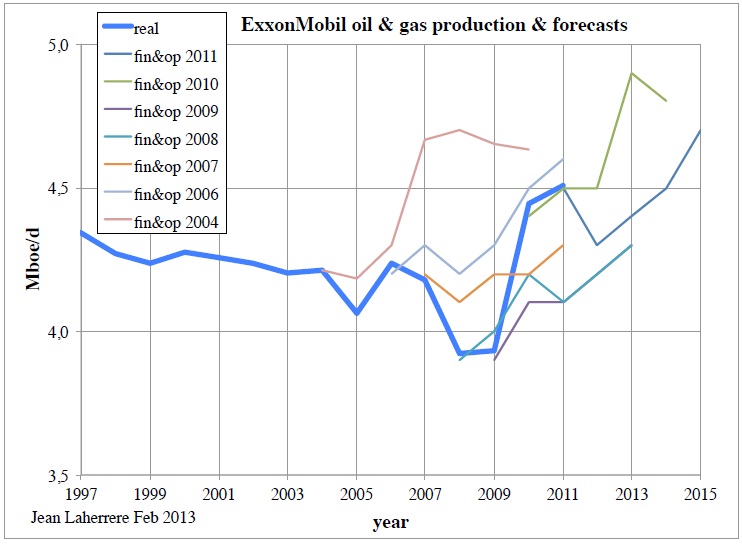

In

his paper on IOCs, Jean also makes the point that production

forecasts of international oil companies have been consistently on

the high side as shown on this graph:

Jean’s

production curve includes gas which has been converted to barrels of

oil equivalent.

Jean’s

production curve includes gas which has been converted to barrels of

oil equivalent.

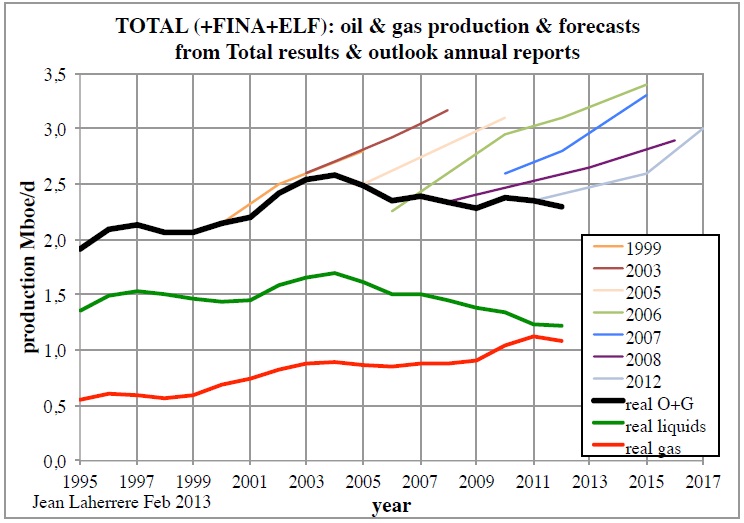

Let’s

have a look at the French oil major TOTAL:

Total’s

oil production peaked in 2004 and declined since then by 4% pa. The

underlying decline rate (declining areas) was also a steep 5.7 % pa.

Total’s

oil production peaked in 2004 and declined since then by 4% pa. The

underlying decline rate (declining areas) was also a steep 5.7 % pa.

This graph from Jean shows declining oil production for TOTAL since 2004

and growing gas production (measured in equivalent oil barrels). In

energy terms, the growth in gas could not offset the decline in oil.

All oil and gas forecasts have been too high compared with actual

production. Upward curves for the future attract investors and keep

shareholders happy.

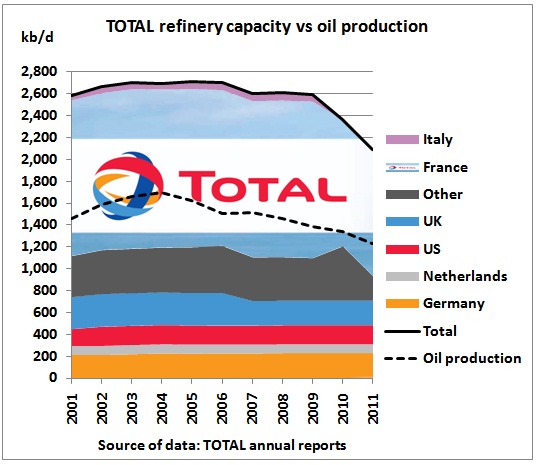

TOTAL seems to adjust their refinery capacity (colored areas) to peaking

oil production (dashed line). Their own oil is sufficient for only

around 58% of their refinery capacity.

All

TOTAL data are from

here:http://www.total.com/en/investors/regulated-information-in-france/annual-reports-922804.html

We

continue with the next oil major, Exxon Mobil

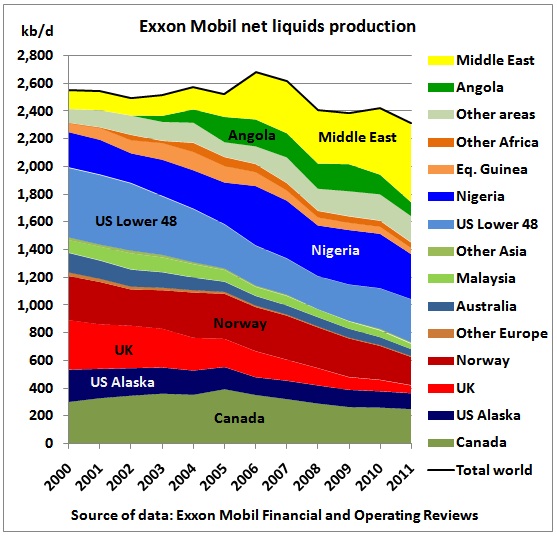

Exxon Mobil’s net liquids production peaked in 2006 and declined since

then at 2.8%. The peak was supported by oil from the Middle East. The

underlying decline rate after 2004 (without Middle East) was 4%

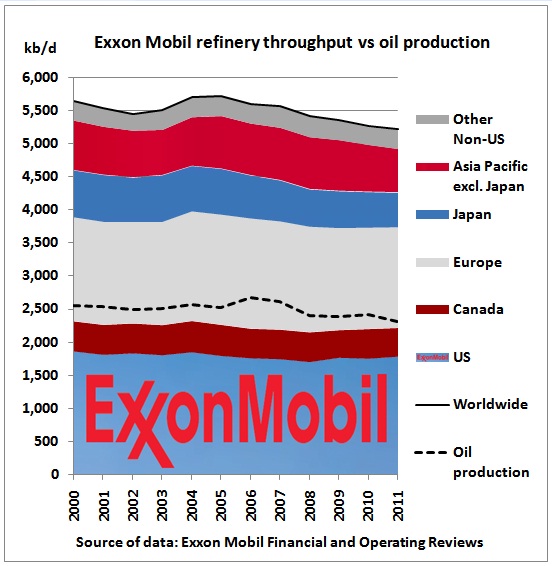

Exxon Mobil’s oil fills only 44% of its refinery throughput. All data are

from here:

On this graph from Jean, Exxon Mobil’s gas production increased as a

result of projects in Qatar and shale gas which more than offset –

in energy terms – declining oil production. Only 2009 forecasts

were lower than actual. 2010 forecasts were correct for 2011.

Chevron’s

production peaked in 2000 but managed to build up a 2nd,

albeit lower peak in 2010, thanks to oil mainly from Kazakhstan,

Nigeria and the US.

It is too early to calculate a reliable overall decline rate after the

2nd peak

but the underlying decline rate of countries with stagnating or

declining production is a modest 3.4 % since 2000.

After selling off the Motiva and Equilon refineries to Shell, Chevron’s

oil production is more or less in line with its refinery inputs, on a

net basis.

Chevron

data are from here (including earlier

reports)http://phx.corporate-ir.net/phoenix.zhtml?c=130102&p=irol-reportsAnnualArchive_pf

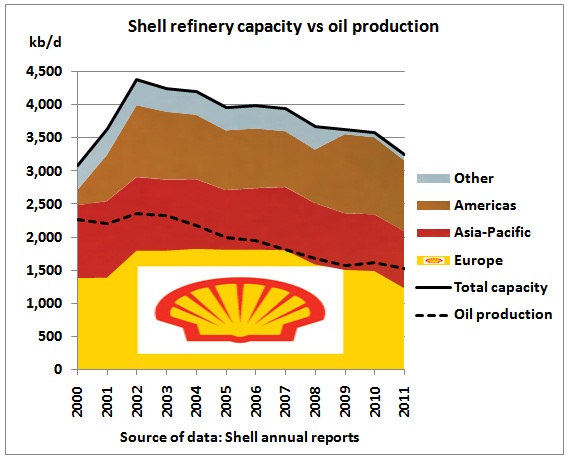

The

last of the 5 majors is Shell which peaked in 2002.Except for very

modest contributions from Russia, Brazil and Nigeria (on a bumpy

plateau), the rest of the supply system is in decline.

The overall decline rate was 3.9 %, and the underlying decline rate 5.4%.

We see the acquisition of refineries in 2001/02, e.g. from Chevron as

mentioned above, but since then Shell’s refinery capacities are

adjusted according to declining oil production, which is just enough

for 47 % of capacities.

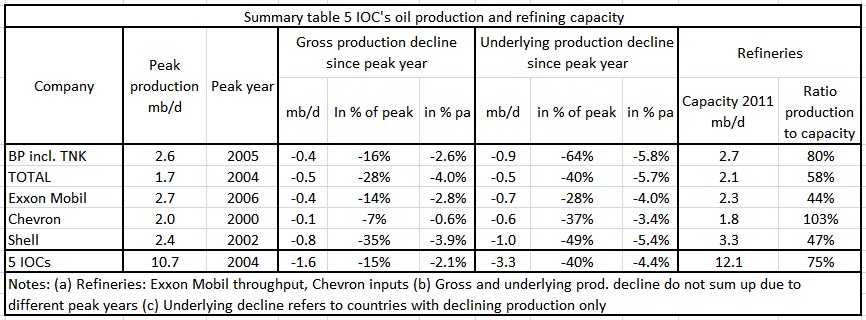

Summary

We

can now add all production graphs, starting the stack with the

underlying decline:

and put the results into a table:

Conclusion:

The

underlying decline rate of production is the most important parameter

for future production and thus refinery utilization. This rate

determines the over-all decline once the growing, offsetting

countries no longer grow. Oil companies with refining capacities

greatly exceeding their own oil production will face cost pressures

as this oil has to be procured from globally available crude exports

which are shrinking. There is no way this system can survive long

without further price increases when demand grows and crude exports

decline. This will have a negative impact on all oil-dependent

infrastructure like toll-ways, airport expansions etc. All such new

projects should be shelved for good.

No comments:

Post a Comment

Note: only a member of this blog may post a comment.