Bank

Run: Deutsche Bank Clients Are Pulling $1 Billion A Day

16

July, 2019

There

is a reason James Simons' RenTec is the world's best performing hedge

fund - it spots trends (even if they are glaringly obvious) well

ahead of almost everyone else, and certainly long before the

consensus.

That's

what happened with Deutsche Bank, when as we reported

two weeks ago,

the quant fund pulled its cash from Deutsche Bank as a result of

soaring counterparty risk, just days before the full - and to many,

devastating - extent of the German lender's historic restructuring

was disclosed, and would result in a bank that is radically different

from what Deutsche Bank was previously (see "The

Deutsche Bank As You Know It Is No More").

In

any case, now that RenTec is long gone, and questions about the

viability of Deutsche Bank are swirling - yes, it won't be insolvent

overnight, but like the world's biggest melting ice cube, there is

simply no equity value there any more - everyone

else has decided to cut their counterparty risk with the bank with

the €45 trillion in derivatives, and according to Bloomberg

Deutsche Bank clients, mostly hedge funds, have started a "bank

run" which has culminated with about $1 billion per day being

pulled from the bank.

As

a result of the modern version of this "bank run", where

it's not depositors but counterparties that are pulling their liquid

exposure from DB on fears another Lehman-style lock up could freeze

their funds indefinitely, Deutsche Bank is considering how to

transfer some €150 billion ($168 billion) of balances held in it

prime-brokerage unit - along with technology and potentially hundreds

of staff - to French banking giant BNP Paribas.

One

problem, as Bloomberg notes, is that such a forced attempt to change

prime-broker counterparties, would be like herding cats, as the

clients had already decided they have no intention of sticking with

Deutsche Bank, and would certainly prefer to pick their own PB

counterparty than be assigned one by the Frankfurt-based bank. Alas,

the problem for DB is that with the bank run accelerating, pressure

on the bank to complete a deal soon is soaring.

Here

are the dynamics in a nutshell, (via Bloomberg): Deutsche Bank CEO

Christian Sewing is pulling back from catering to risky

hedge-fund clients, i.e. running a prime brokerage, as he attempts to

radically overhaul the troubled German lender while BNP CEO

Jean-Laurent Bonnafe wants to expand in the industry.

A

deal of this magnitude would be a stark example of the German firm’s

retreat from global investment banking while potentially transforming

its French rival from a small player in the so-called prime-brokerage

industry to one of Europe’s biggest.

There

is just one problem: nothing is preventing those clients who would be

forcibly moved from a German banking giant to a French banking giant

from redeeming their funds. And that's just what they are doing. Or

rather, nothing is preventing them from moving their exposure for

now,

which is why they are suddenly scrambling to do it before they are

suddenly gated.

Which

is why the final shape of the deal remains, pardon

the pun,

fluid, and it is unclear how it will proceed, facing a multitude of

complexities, including departing clients.

In

an attempt to stop the bank run, BNP executives are meeting with U.S.

hedge-fund clients this week to convince them to stay following

similar sit-downs with European funds last week, Bloomberg sources

said.

It

also means that countless hegde

funds are suddenly at risk of being gated on whatever liquid exposure

they have toward Deutsche Bank.

To

be sure, Deutsche Bank’s hedge fund balances have been declining

throughout the year as speculation swirled around Sewing’s

intentions for the prime brokerage, but the rate of redemptions was

far lower than $1 billion per day. Now that the bank jog has become a

bank run, the

next question is how much liquidity reserves does DB really have and

what happen if hedge funds clients - suddenly spooked they will be

the last bagholders standing - pull the remaining €150 billion all

at once.

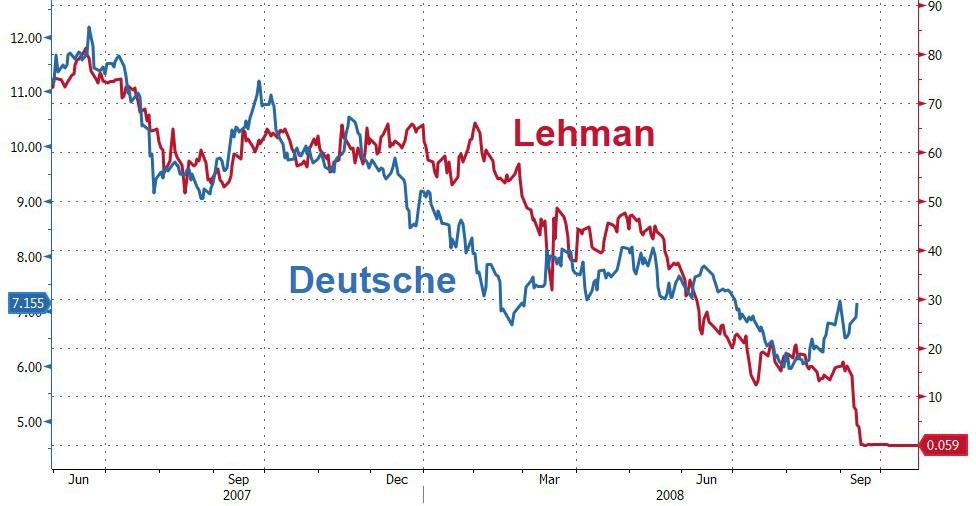

We

are confident we will get the answer in a few days if not hours,

until then please enjoy this chart which compares DB's stock decline

to that of another bank which was gripped by a historic liquidity run

in its last days too…

public's attention, left hand

(EPSTEIN) - While the trick

comes from the right hand

(Deutsche Bank and the

financial system)

HalTurner,

16 July, 2019

Deutsche Bank clients, mostly hedge funds, have started a "bank run" which has culminated with about $1 billion per day being pulled from the bank.

Two

weeks ago,

RenTec, the quant fund, pulled its cash from Deutsche Bank as a

result of soaring counter-party risk in the Derivatives Market, just

days before the full - and to many, devastating - extent of the

German lender's historic restructuring was publicly disclosed.

Questions

about the viability of Deutsche Bank are swirling because everyone

with half a brain knows that Deutsche Bank has billions of euros

worth of derivatives and credit default swaps, which they list on the

balance sheets as liquid assets. They're not liquid - at

all.

This

realization by the financial community big shots has caused Deutsche

Bank's stock price to nose-dive over the past year, to the point

there is simply no equity value there any more. This has

caused almost everyone else to decide to cut their counter-party

risk with the bank that holds €45 trillion in

derivatives it oversees. That means clients, mostly hedge

funds, have started a "bank run" which has culminated with

about $1 billion per day being pulled from the bank.

The

bank announced it was laying off almost 20,000 employees and closing

certain business units to improve the Bank's financial situation but

word got out that as a result of the modern version of this "bank

run" (where it's not depositors but counter-parties that are

pulling their liquid exposure from DB on fears another Lehman-style

lock up could freeze their funds indefinitely) Deutsche Bank is

considering how to transfer some €150 billion ($168 billion) of

balances held in it prime-brokerage unit - along with technology and

potentially hundreds of staff - to French banking giant BNP Paribas.

Deutsche

Bank CEO Christian Sewing is pulling back from catering to risky

hedge-fund clients, i.e. running a prime brokerage, as he attempts to

radically overhaul the troubled German lender while BNP CEO

Jean-Laurent Bonnafe wants to expand in the industry.

A

deal of this magnitude would be a stark example of the German firm’s

retreat from global investment banking while potentially transforming

its French rival from a small player in the so-called prime-brokerage

industry to one of Europe’s biggest.

In

an attempt to stop the bank run, BNP executives are meeting with U.S.

hedge-fund clients this week to convince them to stay following

similar sit-downs with European funds last week.

A

forced attempt to change prime-broker counterparties is doomed

to fail if clients have already decided they have no intention

of sticking with Deutsche Bank. Clients would prefer to pick their

own Primary Broker counterparty than be assigned one by a failing

Deutsche Bank.

With

the bank run accelerating, pressure on the bank to complete a deal

soon is soaring.

HAL

TURNER COMMENTARY

European

Banking laws do not protect Depositors the way American Banking laws

do. In Europe, if a bank fails, DEPOSITORS CAN LOSE THEIR MONEY

but get "equity" (stock) in the failed bank as compensation

during a bank reorganization.

Some

larger Depositors get what is euphemistically called "a Haircut"

meaning they do not even get full stock value for the money they

lose. This is known in the industry as a "Bail-In"

since depositors are the ones who lose and the banks get Depositor

money in the failing bank's pocket.

With

this type of news coming out from Europe today, its a wonder

Depositors are not already lined-up to get their money out of

Deutsche Bank.

You

can rest assured ... that ANYTHING in their 45 TRILLION euro book of

Derivatives that could be sold off for a profit HAS been sold.

You can also be virtually assured that what remains in Deutsche Bank's 45 Trillion EURO derivatives book are losers and hidden losses.

As I have said for years now Deutsche Bank was a DEAD BANK WALKING (their derivatives book told me that) ... and that eventually the German Government was going to have to come in and put in taxpayer money to keep the bank from collapsing (which would severely hurt the German Economy).

ANY depositor in Deutsche Bank would NOW be a fool to leave any uninsured money in that institution ... since you would face the risk of LOSING ALL of the uninsured part of that money.

Once a bank's unraveling begins it tends to accelerate to TERMINAL VELOCITY fairly quickly.

Can the bank in it's present form last until the New Years?

Maybe ... but you wouldn't find my leaving my own money there as we wait to see.

Maybe

this is why German Chancellor Angela Merkel has been seen literally

shaking at public events like this one on June 18 in Berlin, her

whole body visibly shaking as she received the new Ukrainian

president at the chancellery:

Or as shown by NBC News HERE a week later on June 27 while she appointed a new Justice Minister.

Or as seen for the THIRD TIME on July 10 when the German chancellor's body shook back and forth visibly as she stood at a military honors ceremony alongside the visiting Finnish prime minister Antti Rinne:

There is widespread speculation -- only rumors - she may have the inside info about Deutsche Bank and knows that if (when) the bank fails, the German people would likely rise-up and LYNCH HER for it.

The German people would be the least of it. If Deutsche Bank fails, it takes out the €45 TRILLION Derivatives Market and that would smash the global financial system in a way the world has never seen before. It would trigger a global financial meltdown.

No comments:

Post a Comment

Note: only a member of this blog may post a comment.