Forecast 2017: The Wheels Finally Come Off

James Howard Kunstler“There is no other endeavor in which men and women of enormous intellectual power have shown total disregard for higher-order reasoning than monetary policy.

— David Collum

American

Notes

Apart

from all the ill-feeling about the election, one constant ‘out

there’ since November 8 is the Ayn Randian rapture that infects the

money scene. Wall Street and big business believe that the country

has passed through a magic portal into a new age of heroic

businessmen-warriors (Trump, Rex T, Mnuchin, Wilbur Ross, et. al.)

who will go forth creating untold wealth from super-savvy deal-making

that un-does all the self-defeating malarkey of the detested Deep

State technocratic regulation regime of recent years. The main signs

in the sky, they say, are the virile near-penetration of the Dow

Jones 20,000-point maidenhead and the rocket ride of Ole King Dollar

to supremacy of the global currency-space.

I

hate to pound sleet on this manic parade, but, to put it gently, mob

psychology is outrunning both experience and reality. Let’s offer a

few hypotheses regarding this supposed coming Trumptopian nirvana.

The

current narrative weaves an expectation that manufacturing industry

will return to the USA complete with all the 1962-vintage societal

benefits of great-paying blue collar jobs, plus an orgy of

infrastructure-building. I think both ideas are flawed, even allowing

for good intentions. For one thing, most of the factories are either

standing in ruin or scraped off the landscape. So, it’s not like

we’re going to reactivate some mothballed sleeping giant of

productive capacity. New state-of-the-art factories would require an

Everest of private capital investment that is simply impossible to

manifest in a system that is already leveraged up to its eyeballs.

Even if we tried to accomplish it via some kind of main force

government central planning and financing — going full-Soviet —

there is no conceivable way to raise (borrow) the “money” without

altogether destroying the value of our money (inflation), and the

banking system with it.

If

by some magic any new industrial capacity were built, much of the

work in it would be performed by robotics, not brawny men in blue

shirts, and certainly not at the equivalent of the old United Auto

Workers $35-an-hour assembly line wage. We have not faced the fact

that the manufacturing fiesta based on fossil fuels was a one-time

thing due to special historical circumstances and will not be

repeated. The future of manufacturing in America is frighteningly

modest. We’ll actually be lucky if we can make a few vital

necessities by means of hydro-electric or direct water power, and

that will be about the extent of it. Some of you may recognize this

as theWorld

Made By Hand scenario.

I’ll stick by that.

Similarly

for “infrastructure” spending touted by the forces of Trump as

the coming panacea for economic malaise. I suspect most people assume

this means a trillion-dollar stimulus spend on highways and their

accessories. Well, that also assumes that we expect another fifty

years of Happy Motoring and suburban living. Fuggeddabowdit. We’re

in the twilight of motoring anyway you cut it, despite all the

chatter about electric cars and “driverless” cars. We won’t

have the electric capacity to switch over the Happy Motoring fleet

from gasoline. The oil industry itself is already headed for collapse

on its sinking energy-return-on-investment. And our problems with

money and debt are so severe that the motoring paradigm is more prone

to fail on the basis of car loan scarcity and unworthy borrowers

before the fueling issues even kick in. Every year, fewer Americans

can afford to buy any kind of car — the way they’re used to

buying them, on installment loans. The industry has gone the limit to

help them — seven-year loans for used cars! — but they have no

more room to maneuver. The car financing system is broken. Bear in

mind the original suburbanization of America back in the 20th century

— along with its accessory automobiles — must be regarded as the

greatest misallocation of resources in the history of the world.

So, a rebuild of all this stuff would represent more and possibly

even greater malinvestment. We could have applied our post-WW2

treasure to building beautiful walkable towns and cities with some

capacity for adaptive re-use, but we blew it in order to enjoy life

in a one-time demolition derby. Life is tragic. Societies make poor

choices sometimes, and then there are consequences.

We

also might have been in better shape now if, beginning twenty years

ago, we began a major rebuild of our railway infrastructure. But we

blew that off, too, and shortly it will be very difficult to get

around this geographically large country by any mechanical means. It

may be too late now to do anything about that for the financing

reasons already touched on — and which I will elaborate on next.

The bottom line is that President Donald Trump will be overwhelmed by

a sea of financial troubles from the very get-go, and here’s why.

Designated

Bag-Holder

The

American people have been punked by their own government and their

central bank, the Federal Reserve, for years and the jig is now up.

In 2017 both will lose their authority and legitimacy, a very grave

matter for the survival of this republic.

Insiders

surely have seen this coming for a long time. The people running this

so-called Deep State of overblown and overgrown institutions probably

acted at first with the good intentions of keeping the national

lifestyle afloat. But in the end (now approaching) they stooped to

too much duplicity and deceit in the desperate attempt to not just

preserve the system, but to protect their own reputations and

personal perquisites. And now there ought to be some question with

the election of 2016 that they have engineered all of this system

fragility to blow up on Mr. Trump’s watch, so they can blame him

for it. It was going to blow up anyway. But had Hillary Clinton won

the election, at least the right gang would have had to take the

blame — the people in charge for the past twenty years. Instead,

Donald Trump has been elected Designated Bag-Holder.

About

That “Big Fat Ugly Bubble” and its Consequences

Part 1:

History Lesson

The

USA ran out of growth capacity around the turn of the millennium

because we ran out ofaffordable energy

to run our techno-industrial economy. It was hard to see this with

seemingly plenty of oil available. And, of course, the computer tech

fiesta was blossoming, but for all that glitzy stuff to attract

dwindling real capital, other old stuff had to go, and did go, and

when all was said and done the computers did not generate much wealth

or social value. In fact, the diminishing returns and blowback of

computer tech were arguably more damaging than beneficial to society

and its economy. Look at where the middle class is today. Computer

tech gave the magical appearance of growth while actually undermining

it.

By

affordable energy I mean energy with a greater-than 30-to-one

energy-return-on-investment, which is the ratio you need for the kind

of life we lead. That’s what the now-ridiculed Peak Oil story was

really about: not running out of oil, but not getting enough bang for

our bucks pulling the remaining oil out of the earth to maintain our

standard of living. I’ll return to this issue in more detail later.

But that was what provoked America’s 21st century

economic malaise. Everything we’ve done in finance since then has

been an attempt to compensate for our fundamental problem with debt —

borrowing from the future to maintain our current (unaffordable)

standard of living. Our debt has grown ever larger and faster each

year, and our methods for managing it have become more desperate and

dishonest as that occurred.

The

culprit at the center is America’s central bank, the Federal

Reserve, which is actually not a government agency as it seems, but a

consortium of the nation’s biggest private banks, lately known as

Too-Big-To-Fail. The Fed was created in 1913, when the complexities

of capital finance were multiplying in step with the complexities of

industrial production, which, remember, was a new and evolving

phenomenon of human history. Mankind had no prior experience with

industrialism. We discovered toward the end of the 19th century

— decades of unprecedented industrial growth — that the system’s

dynamic produced booms accompanied by very destructive busts.

The

operations of banking usually outran the cycles of trade, industry,

and war that were coloring evolving Modernity. So the Fed was created

to smooth out these cycles. It had two basic mandates for this:

acting as the lender of last resort between banks during financial

panics so that some money would always be available in an emergency;

and stabilizing the money supply and prices in the system. The Fed

failed spectacularly to smooth out the cycles of boom and bust and to

maintain the value of the dollar over time.

Sixteen

years after the Fed’s creation, America entered its worst economic

downturn ever, the Great Depression, which was only mitigated by the

colossal abnormality of World War Two. America emerged from that

episode as the last industrial society standing amid everyone else’s

smoldering ruins.

That gave us an extraordinary advantage in world

trade lasting roughly thirty years. That high tide of the era of

seeming “normality” — the 1950s and 60s, which the

Trumpian-minded might recall as “great” — started unraveling in

the 1970s, which was not coincidentally the moment of America’s

all-time oil production peak.

In

1977, the Fed was given a third mission of promoting maximum

employment with a trick-bag of tools for manipulating the money

supply and credit creation that have proven to be fatally

mischievous. This new task elevated Fed officials, and especially its

chairperson, to the status of viziers — magicians using occult

mathematical models and formulas — to cast spells capable of

controlling the macro economy the way wizards are thought to control

external reality. Their pretenses seemed to work for reasons

unrelated to the spells they were learning to cast.

It

is still largely unrecognized that America recovered from the

financial disorder of the 1970s not because of the charms of

“Reaganomics” but for the simple reason that the last giant finds

of oil with greater than 30-to-one energy-return-on-investment came

on line in the 1980s: Alaska’s North Slope, Britain and Norway’s

North Sea fields, and Siberia. That allowed the USA and the West

generally to extend the techno-industrial fiesta another twenty

years. As that bounty tapered down around the year 2000, the system

wobbled again and the viziers of the Fed ramped up their magical

operations, led by the Grand Vizier (or “Maestro”) Alan

Greenspan, who worked the control rods of interest rates as though

the financial system were a great nuclear powered pipe organ that

could be revved up and tamped down by a wondrous Fed control panel.

This period of Fed spell-casting was characterized by ever more

systemically complex finance, growing systemic fragility, pervasive

institutionalized accounting fraud, and ever-greater bubbles and

busts. Deregulation, especially the 1998 repeal of the Glass-Steagall

Act of 1932, sealed America’s financial fate.

Debt

was the meat-and-potatoes of the Fed’s wizardry, but the “secret

sauce” of Fed magic was fraud, in the form of market interventions,

manipulations, regulatory negligence, and just plain systematic lying

about the numbers that defined the economy. It amounted to

nationalized financial racketeering.

Under the consecutive Grand

Vizierships of Greenspan and Ben Bernanke, control fraud (using

official authority to cover up misconduct) was perfected by banking

executives, eventuating in the mortgage securities fiasco of 2008,

which took down the housing market and the economy. (That housing

market, by the way, was made up mainly of suburban houses, the sine

qua non of the

greatest misallocation of resources in the history of the world.)

Of

course, nobody paid a criminal penalty for any of this misconduct

besides the maverick Ponzi artist Bernie Madoff, and a few other

small fish. The regulators looked the other way, on orders from their

bosses. Unlike the earlier Savings and Loan bank crisis of the late

1980s, none of the leading bank officer perps went to jail. The

damage of the 2008 crash was epic and never repaired, only papered

over with more debt, more deceit, and more racketeering.

The

supposed remedy, the Dodd-Frank Act of 2010, was a cover for

continued pervasive fraud and the institutional “capture” of

government by the banking industry and its handmaidens, really a

fascist melding of banking and government, a swindle machine in which

anything goes and nothing matters.

The frauds have only been

rechanneled since 2008 into college loans, car loans, corporate stock

buyback monkey business, currency arbitrage shenanigans, private

equity asset-stripping, and the gigantic black box of derivatives

trading.

About

That “Big Fat Ugly Bubble” and its Consequences

Part 2:

2017, the Year of Living Anxiously

Under

Bernanke’s successor, UC-Berkeley Professor Janet Yellen, the

emphasis in Fed policy has been an elaborate game of “data-dependent”

foot-dragging — a lot of talk with no action — with the data

itself largely fraudulent, especially the easily gamed employment and

GDP numbers that supposedly determine the rise or fall of interest

rate policy. In short, the racketeering continues while the

authorities quail in the face of accumulated and now inescapable debt

quandaries ever more certain to end in systemic collapse.

Get

this: the Fed is completely full of shit. It is terrified of the

conditions it has set up and it has no idea what to do next. The

“data” that it claims to be so dependent on is arrantly fake. The

government’s official unemployment number at Christmas 2016 was 4.6

percent. It’s a compound lie. The 4.6 percent does not include the

95 million people out of the workforce, most of them able-bodied, who

have simply run through their unemployment benefits and given up

looking for work. Nor does it figure in the fact that roughly 90

percent of the new jobs created are part time jobs, many of them held

by people working several jobs (because they have to, to pay the

bills). Nor does it detail the quality of the jobs created (minimum

wage shit jobs.)

That

4.6 unemployment figure is the main pillar of the Fed’s “data.”

They interpret it as meaning the economy is roaring and has their

full confidence.

They‘re lying about that, of course. They have

been touting “the recovery” (from the crash of 2008) continually

and heralding a program of “normalizing” interest rates upward

for two years. In 2015 they didn’t do anything until the very last

Fed meeting of the year when they raised the Fed Funds rate 25 basis

point (that’s a measly one-quarter of a percent). They raised, they

said, because they were “confident” about the economy. No, that’s

not why. They did it because they talked about it all year without

doing anything and their credibility was on the line. They also

promised four rate hikes altogether in 2016, which they then failed

to carry out.

After

that December 2015 rate hike, the stock markets tanked 10 percent. By

springtime, the markets appeared to be bouncing back, so the Fed

started talking about more rate hikes again. They talked it up all

year without acting, an impressive act of fakery. The surprise Brexit

vote gave them the heebie jeebies. They laid low. Meanwhile, the US

election season was on. The Fed denies this, but they did not raise

interest rates for eleven months in 2016 solely because they wanted

to make the Democratic administration look good heading into the

November vote, and they knew the economy was fragile. Once Hillary

was nominated they were determined to usher her into the White House

on a high tide of fake good economic news.

When

she lost the election the stock markets surprised everyone by

entering a super-bubblicious Trumpxuberance rally. There is a

narrative for that too in the media chatter and it is simpleminded

nonsense based on the sheer hope that Trumponomics will be great for

business. More on that below.

Roaring

stock markets were a secondary pillar of the Fed’s economic

world-view. The post-election 2000 point upsurge in the Dow, along

with the historically low 4.6 unemployment number, gave the Fed the

opportunity on December 15 to do the same thing they did the previous

year: cover their asses and preserve some credibility by hiking the

Fed Funds rate one-quarter percent. You’d think if they were really

confident in the economy — especially given the year–end rally —

they would venture to raise by half a percent or more. They are not

confident. They are lying with their fingers crossed.

The

Fed Funds rate is one thing. As it happens, the Fed does

not directly control

the interest rates on US treasury bonds, and they have been rising

shockingly through the second half of 2016. The crucial ten-year

treasury rate has gone up a hundred percent since the summer. Because

bond values move inversely to bond rates, the price of treasuries has

tanked, inducing trillions of dollars in losses to bond-holders

around the world. The bond market is many times larger than the stock

markets. Bonds have been in a bull market since the early 1980s and

that bull rolled over in mid-2016. A bear market is now on, meaning

bond-holders are dumping their bonds. China and Saudi Arabia are

among the leading dumpers of US Treasuries because they need the

money for one reason or another. They will dump more in 2017 because

both countries are in deep economic trouble. Too many bond sellers

and not enough buyers in the market drive interest rates up. Rates

have a lot room to move up, since they started at near-zero.

Accordingly, their value has a long way to fall.

Bonds,

of course, represent debt. Total US debt has doubled under President

Obama from around ten trillion to twenty trillion dollars (as it

doubled under Bush Two from five to ten trillion dollars). The

reason, as stated above, is that we don’t produce enough to cover

the cost of our national way of life, so we have to borrow

continually at ever-greater volume. Every year, the Treasury has to

pay interest on all that debt. It’s a lot of money. This year, with

interest rates starting out at historically unprecedented lows (not

seen ever in recorded history), the Treasury paid over a

quarter-trillion dollars in interest.

By the way, the government

borrows money to make these interest payments too. An interest rate

rise of one percent, would drive the annual US debt higher by $190

billion. As the late, great Senator Everett Dirkson (R-Ill) once

pungently remarked: “…a billion here, a billion there, sooner or

later you’re talking about real money.”

A

sharply rising interest rate on the ten-year Treasury bond will

thunder through the system. A lot of other basic interest costs are

keyed to the ten-year bond rate, especially home mortgages, apartment

rentals (landlords hold mortgages), and car payments. When the ten

year bond rate goes up, so do mortgage payments. When mortgage rates

go up, house prices go down, because fewer people are in a position

to buy a house at higher mortgage rates, and rents go up (more

competition among people who can’t buy a house). Zero Interest Rate

Policy (ZIRP), in force for ten years, has driven house prices back

to stratospheric levels. They are now primed to fall, perhaps

severely, leaving many homeowners “underwater,” with houses worth

way less on the market than the amount of mortgage left to pay off.

The re-financing market is dead. Housing starts were already down by

a stunning 19 percent in November. Automobile sales are rolling over.

Manufacturing and retail sales numbers are down at year end. What’s

up: stocks, stocks, stocks.

Yet

investors did not execute the usual end-of-year profit-taking in the

expectation that Trump would lower the capital gains tax in 2017, so

why sell now? You can wait until January 3, 2017 to sell, and then

not have to pay tax on your profits until April of 2018. Will

investors start dumping in the first trading days of 2017? I think

so. And will that selling beget a stampede for the exits? And what

will happen if the interest rate on the ten-year bond hits three

percent? (It doesn’t have far to go). Or maybe even four percent?

What happens is the stock markets go down in the first quarter of

2017. My forecast is 20 percent down on the S & P. That will only

be a preview of coming attractions once Trump gets his mitts on the

levers of power. A still bigger crash ahead later in the year!

Why

Trump Can’t Pull a Reagan

When

Reagan came into office in 1981, inflation was raging largely because

of the effects of the oil crises of 1973 and 1979, which had produced

the “stagflation” that confounded the reigning economists’

models (they knew nothing about the relationship between energy

dynamics and capital formation). The Fed Funds rate was almost 20

percent in 1981. It had a lot of room to move down. The national debt

was less than one trillion (Reagan eventually ran it up to $2.8

trillion). Reagan was able to endure a sharp recession early in his

first term — and voodoo economics got him through all the rest of

his tenure, with both inflation and interest “normalizing” — as

mentioned earlier, he enjoyed the bonanza of the last great non-OPEC

oil discoveries coming on-line during his two terms, which ramped up

economic activity and growth.

Today,

the US is in a box and Trump comes on the scene with nowhere to move.

Too much debt can only be managed if interest rates are kept low.

Everybody and his mother around the world is dumping US Treasuries.

With a bear market in bonds on, the Fed as buyer of last resort will

have to sop up whatever comes on the market to keep the interest rate

from rising above three percent on the ten-year, and even that may

not prevent it. Trump’s vaunted infrastructure stimulus plan will

be impossible to carry out without the Fed monetizing the necessary

debt. So stimulus implies bigger deficits, which means more bonded

debt that nobody wants to buy. The result will be inflation and

accordingly further upward pressure on interest rates. Higher

interest rates, in turn, will negatively impact economic activity,

lowering tax revenue, inducing larger fiscal imbalances and greater

instability.

Trump

may never even get the stimulus he seeks. The Republican

controlled-congress has vowed not to increase the national debt. How

can Trump fulfill his pledge to cut taxes and bring on stimulus

without hugely increasing the debt? If there is war over spending

between Trump and Congress, Congress is likely to win, since they

control the fiscal purse strings. Of course, Donald Trump cannot

abide not winning. Hostilities between them may become permanent

early in Trump’s term and bring on even more dangerous paralysis of

governance.

Also

early in 2017, the Fed will abandon its “dot plot” talk about

further interest rate hikes. They may also surrender their

credibility in the process.

The system can’t take the strain of

three interest rate rises in 2017. It may be that Janet Yellen has

raised the Fed Funds rate a total of one-half a percent in two years

solely to be able to lower them again when the real economy finally

tanks under that strain of incessant central bank chicanery. By the

second quarter of 2017, following a 20 percent stock dump, the Fed

will start making noises about Quantitative Easing 4 (QE), or they

will cook up some other program that accomplishes the same thing

under a new cockamamie label. More QE (or something like it) will

drive the dollar back down and gold back up. The housing market will

be in the toilet and the rest of the economy will follow it down the

drain. By the end of Trump’s first year in office, there will

another, greater, dump in the stock markets after the initial 20

percent drop in the first quarter. America will be great again, all

right: we’ll be entering a depression greater than the Great

Depression of the 1930s.

Desperate

Measures

One

of the other big and dark trends of the past year has been the move

of governments around the world — and among the economist /

necromancers who advise them — to ban cash from the scene in order

to herd all citizens into a digital banking system that will allow

the authorities to track all financial transactions and suck every

possible cent of taxes into national coffers. It would also be an

opportunity for the bank-and government cabal to impose negative

interest rates (NIRP) on bank accounts so that money herded into the

digital system could be surreptitiously “taxed” by charging

account holders just for being there (against their will). It’s a

little hard to see how that might happen just now in a broad rising

rate environment, but it would be the natural accompaniment to

banning cash — and renewed aggressive QE

(QE forever!) might do the trick.

Harvard

economist Kenneth Rogoff literally wrote the book on this (The

Curse of Cash;

Princeton University Press, 2016), a mendacious argument that cash

money merely enables drug dealers and terrorists to operate and has

no useful place otherwise in a regular economy. Rogoff appeared to be

angling for the Treasury slot in Hillary’s cabinet, and would have

fit in perfectly with this totalitarian assault on the public’s

financial liberty — but, as we know, Hillary didn’t make it.

Efforts

to eliminate cash are already underway around the world. The EU

officially discontinued the €500 note from circulation. Ken

Rogoff’s Harvard colleague, Larry Summers, was calling for

abolition of the $100 bill a year ago. Sweden is successfully herding

its people out of fiat krona. India’s Prime Minister Narendra Modi

pulled a fast one in November by banning the 1000 and 500 rupee note

(worth respectively $14 and $7), and threw India’s economy into a

epileptic seizure. The idea was to discipline tax evaders who operate

in a cash economy. The catch was that more than 85 percent of India’s

economy operates on a cash basis among people too poor to have bank

accounts and credit cards — including millions of truck drivers and

ordinary laborers. Naturally, the Indian economy froze. Nobody could

get paid. Food rotted in stalled trucks. ATM withdrawals were limited

to a few day’s walking-around-money. Citizens could not even

exchange their 1000 and 500 rupee notes at the banks without going

through onerous time-consuming bureaucratic rigmarole, including

fingerprinting and the submission of tax records. The process caused

discouraging long queues to form at the banks, and was probably

designed to discourage the exchange of the 1000 and 500 rupee notes

altogether and instead just retire them from circulation — which

means a lot of poor people lost the minimal cash savings they had.

It’s

hard to see the US government banning cash as clumsily as India did,

but they have other ways to herd the multitudes into the black box of

all-digital banking. Financial author James Rickards calls this the

“Ice-Nine” program, in reference to the isotope of water in Kurt

Vonnegut’s sci-fi novel Cat’s

Cradle that

freezes the world in a horrifying chain reaction. Rickards’

Ice-Nine financial nightmare would include features like freezing

bank accounts, bail-ins (confiscation of accounts), limits on ATM

withdrawals, and the “gating” of investment funds. Ice-Nine would

be invoked in a banking emergency — say, a derivatives “accident”

that took out some Too-Big-Too-Fail giant, or really anything that

triggered the extreme fault lines in the ultra-fragile system that

the world’s money elites have cobbled together to keep the garbage

barge of global finance from sinking. In his recent book, The

Road to Ruin,

Rickards reminds readers that the emergency act signed by Bush Two

after 9/11 has remained in effect under Obama, so that America is

“just one phone call away from martial law.”

Another

method for depriving citizens of their financial liberty would be for

the government to declare that retirement accounts had to contain a

set percentage of US Treasury paper — once again herding people

into a financial corral against their will — in order to prop up

the value of bonds and tamp down interest rates. David McAlvany (his

excellent podcast here)

makes the interesting point that if herding the public into the

digital financial corral was a key ingredient to “making America

great again,” who could object? — because now you’d be opposing

American greatness! Trump inherited a much bigger problem than Barack

Obama did in 2009. Obama still had enough soft-soap left in the

machine to blow more bubbles. Trump arrives on the scene with the

machine out of bubble-blowing mojo. He’ll be overwhelmed by

financial disorder in 2017 and then the nation’s focus will turn to

a tumultuous political scene

Wild

in the Streets

The

public is just plain pissed off, and remains pissed off after the

Trump Victory. Their anger has been fermenting for decades as their

economic prospects dwindled and they began to understand how it all

worked against them. The battered middle class might have gotten a

temporary thrill from the election, but an awful lot of them are

still out of work, or working at the humiliating shit-jobs that

replaced their old lost jobs in the old real stuff economy. Worse is

coming their way in 2017. Theirs is a true existential crisis.

Even

under the most favorable circumstances, a stimulus program would not

likely get out of congress until much later in 2017, and I personally

doubt that it will get through at all. The so-far-fortunate retirees

plugged into pensions represent another potential trouble spot.

Pension funds are going bust all over the country from the incapacity

to stay solvent in a near-ZIRP environment. In 2016, fissures started

to show in places like the Dallas Police and Firemen’s Pension

fund, when pensioners’ redemptions were shut down. There are

pension funds all over the country floundering from the same

conditions, since the Fed took the “fix” out of “fixed income.”

In the absence of decent “yield,” the pension funds have been

herded into risky stock markets, and if those markets blow up, the

pension funds are going to blow with them… and then the pensioners’

lives are going to blow up… and then maybe civil order dissolves

around the country.

That

may be the moment when President Trump and his militarily-weighted

cabinet appointees opt for martial law. What a goddamned mess that

will be. There is no civilized country on earth with as many small

arms per capita than the USA, and despite the fearsome appearance of

militarized police forces, you cannot overstate how much deadly

mischief a small number of pissed-off people can make with automatic

rifles, rocket-propelled-grenades, Semtex plastic explosive, and

other fun stuff. It could morph easily to a literal war on bankers

and Wall Street in particular, especially if Ice-Nine goes into

effect. Bear in mind that a lot of veterans of the endless Middle

East wars belong to this suffering economic class, and they actually

have some training in the warrior arts.

Their

political counterparts in the Democrat / Prog coastal elite, hardcore

Hillary, PC-and-unicorn crowd are moving through their post-election

Kubler-Ross Transect-of-Grief from denial to anger too. So both sides

are quite pissed off and primed for conflict. The Left will certainly

do everything possible to oppose Trump and try to make him look bad,

whether it’s in the public interest to do so or not. They will

throw every monkey-wrench possible into the machinery of governance,

up to and including the (mostly Democratic Party weighted) Federal

Reserve hierarchy, whose interest rate “dot plot” could be

truly a

plot to

exact revenge on Trump. Of course, that would blow up in their faces

since proportionately the coastal elites own much more stock than the

Trumpenlumpenprole red-staters, and they could be wiped out in a

significant market crash triggered by rising interest rates. But

that’s the thing about political rage: it’s the opposite of

rational.

There’s

no sign that the Democrat / Progs have recognized that their

poisonous identity politics played a significant role in their

electoral defeat. They will not abandon that endeavor in 2017. They

will double-down on it. And as that happens, the Democratic Party

will go the way of the Whigs in 1856 — with a whimper, not a bang.

God knows who or what will replace them as a credible opposition to

Trumpist crypto-Republicanism, although Trump himself stands a good

chance of leading that party to oblivion, too, if my forecast of a

big financial blow-up comes to pass.

The

Red Guard-like action on campus may continue, though it’s hard to

imagine the “Snowflakes” besting their infantile hijinks of 2016.

What they are demonstrating now is that coercive identity politics is

just a new form of leisure-time recreation on campus, like Ultimate

Frisbee and the beer blasts of old! Have fun wrecking faculty careers

and basking in the Facebook feed! A few still-sane people of all

political persuasions are sick of their censorious attacks, reckless

persecutions, and insults to reality — such as the mandatory “white

privilege” trainings and gender identity personal pronoun crusades.

I predict that there will be a revolt among the university trustees

and boards of directors against college presidents and deans who

pander to the Maoist hysteria, as the damage to higher education and

intellectual freedom more generally finally manifests in dropping

enrollments and the loss of public funding.

There

is every sign that black and white racial conflict will grow worse in

the year ahead. The week after Christmas 2016 saw an impressive

number of shopping mall mass melees of black teens all over the

country. For years, the media went along with the hyperbolic story

that innocent black men were being killed by police for no reason —

when the overwhelming majority of those cases involved victims

brandishing guns or grossly misbehaving in some way liable to get

themselves in trouble. Victimology still rules in America. It’s a

psychological defense mechanism to relieve the Dem / Prog’s shame

and anxiety with the outcome of the long civil rights campaign —

namely, black family disintegration, educational failure, and a

shocking rate of black-on-black murder. A subsidiary grievance

industry, lately led by Black Lives Matter, fans the flames of

vengeance against the universal villain, Whitey, whose “privilege”

keeps other people down (except, notice, immigrants from China,

Korea, Vietnam, India, and other places where Whitey is absent.)

So,

now Left and Right are both equally pissed off. It also means you

have two adversarial groups who might give themselves permission to

turn violent to justify their grievances. If the financial markets

tank and the economy freefalls, it is easy to imagine the potential

for violent conflict between the Dem / Progs with their Black Lives

matter proxies against the Trumpista lumpenproles. It would be a

terrible tragic distraction from the business of repairing the common

weal, the economy, and the common culture — but so was the Civil

War

The

Oil Quandary

The

reports of Peak Oil’s death are exaggerated, to borrow a gag from

Mr. Twain. It’s just been playing out in ways that many of us

didn’t quite anticipate and it is still at the heart of our

economic predicament — which is that you can’t rationalize an

annual debt growth rate of 8 percent if your actual economic growth

rate is under 4 percent (paraphrasing Chris Martenson atPeak

Prosperity.com).

We

haven’t run out of oil, but we have run out of oil that is

rationally economical to pull out of the ground. The so-called “shale

oil miracle” extended the oil age a few years by debt-financed

legerdemain. Yes, we drove US oil production way up, almost back up

to the 1970 peak production level around 10 million barrels-a-day

(b/d). The trouble was that the companies producing it didn’t make

a red cent in the process. They just ran up a huge amount of debt to

pursue the shale project. The pursuit was on wholeheartedly beginning

around 2006, because 1) the Peak Oil story was scaring folks,

including folks in the oil industry, and 2) the market price of crude

oil soared after 2004 and shale looked like a possibly winning

venture — especially since conventional exploration in recent years

was turning up almost nothing of significance.

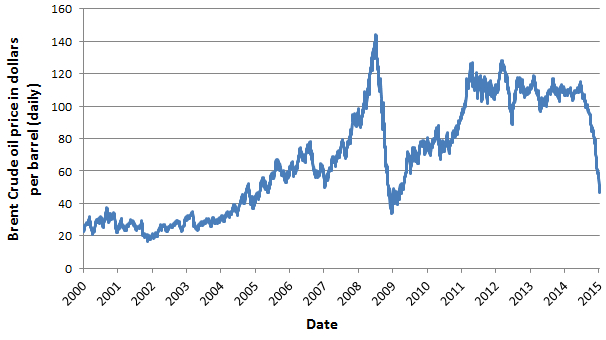

From

2004 the price of oil skyrocketed from around $40-a-barrel until

2008, when it reached a high point of about $140-a-barrel. Then, of

course, the price crashed catastrophically for a year, along with

Wall Street and the economy. But, by then, the fracking industry was

all ramped up in the Bakken fields of North Dakota and the Eagle Ford

range of Texas. Plus the industry was learning some additional new

fracking tricks to goose more oil out of the “tight” rock. So

they were full of confidence, despite the price crash. Then, in 2009

the oil price turned sharply upward again — with central bank ZIRP

and QE and other maneuvers to prop up the economy with more debt at

lower interest rates. And the price of oil just climbed and climbed

again back into the $110-plus range in 2011, and lingered there until

2015, when it crashed again.

Of

course, most of the producers weren’t making any money even at the

$110-a-barrel, but they expected improved technology to mitigate that

eventually. In the meantime, they just produced too much shale oil

and the market was flooded and OPEC got into the act and pumped

all-out trying to crash the price further to put the US shale

producers out of business, and then nobody made a red cent fracking

for shale oil. So, you can see there was a pattern.

The

pattern nicely describes the dynamic advanced by Joseph Tainter in

his seminal work, The

Collapse of Complex Societies:

namely that over-investments in complexity lead to diminishing

returns. That is, as you keep making your systems

extra-hyper-complex, you get less value back for doing it, until you

get to the point where there’s no benefit whatsoever, and then the

system implodes. And that is exactly what has happened with oil and

the economy that was engineered to run on it, and the financial

system that evolved to manage the wealth it used to produce.

A

few other things happened the past few years on the oil scene. The

American oil companies bowed out of Arctic drilling. The Canadian Tar

Sands went bust. The overthrow of Muammar Gaddafi choked off Libyan

production, which was offset by Iran coming back onto the

international market, which was offset by political mischief in

Nigeria that choked off production, which was offset by increased

Iraqi production, which was offset by the collapse of Venezuela. Most

of the world’s oil producers had entered decline anyhow.

Don’t

be fooled. The low prices at the gasoline pumps only mean that US oil

companies are going broke fast, as are American “consumers.”

There’s a basic equation I’ve repeated a few times on this

blog:

oil

over $75-a-barrel destroys industrial economies; oil under

$75-a-barrel destroys oil companies

.

That’s were things stand when the energy return on investment falls

to 5-to-1, as is the case with shale oil. Steve St. Angelo over at

the SRSRocco

Report makes

the excellent point that it takes at least 30-to-1 energy return on

investment to maintain plain vanilla modern life. Anything below that

and parts of the economy have to be sacrificed. Trucking, air travel,

commuting, theme park vacations, your job…. It’s just another way

of describing the pernicious effects of the diminishing returns of

over-investments in complexity.

In

the fall of 2016, OPEC members tried again to agree on an oil

production output limit, as they have done many time before. Each

time, they all managed to cheat in order to sell greater volumes of

oil and make more short-term money — a classic Tragedy

of the Commons story.

Consequently, the price of oil went up to about $53-a-barrel by

Christmas 2016. Don’t expect that to last. Unless, of course, there

is a geopolitical event somewhere out on the oil scene, most likely

in the Middle East, though Venezuela’s economy is approaching total

collapse. The forecast here is for oil prices to follow the stock

markets down in the first quarter of 2017. A lot of junk bonds in the

oil space will default as a result, leading to a general crisis in

shale oil investment.

Vagrant

Thoughts on Geopolitics

As

I write just before New Year’s Eve, President Obama is trying to

start World War Three with Russia as a parting gift to the voting

public. I’m among the skeptics who think that the “Russia Hacks

Election story” is a ruse to divert the public’s attention from

the stupendous failure of the Democratic Party to win, as expected.

Rather, Wikileaks should get the Pulitzer Prize for revealing so much

about the nefarious workings of the Clinton Foundation and the

Democratic National Committee.

Regular

readers know I didn’t vote for Trump, that I heaped considerable

abuse on him in the campaign commentaries. But I didn’t take any

comfort in the nostrum about being “better off with the Devil you

know (Hillary) than the one you don’t know (Trump).” Both

candidates were awful, and the condition of the country is pretty

awful as we turn the corner onto 2017. Readers also know from these

commentaries and from my books that I expect we will have to make big

changes in our living arrangements up ahead as the techno-industrial

fiesta winds down. I won’t reiterate the particulars here, but 2017

is the hinge year for that. The strains on global finance are so

spectacular that something’s got give. President Trump is sure to

be overwhelmed by epic dislocations in markets, currencies, debt, and

misguided central bank efforts to hold back the tides of a necessary

re-set — a re-set which will see a lot of wealth vanish and a lot

of pain inflicted on the losers of wealth, including whole societies.

We

have three major European elections to look forward to in 2017: The

Netherlands and France in the Spring, and Germany in the fall. Geert

Wilders (a member of the Trump Big Hair Club), is virulently against

the “Islamisation” of his country. He has campaigned previously

to leave the European Union and for the return to the old guilder

currency. Should the right-wing Marine LePen win in France, the EU

experiment will likely end — she has made express promises to take

France out of the EU. Angela Merkel has made herself impressively

unpopular by opening the gates to a flood of immigrants fleeing the

breakdown zones of the Middle East and Africa. And then, because of

the Schengen Agreement (free passage across EU borders), the

immigrants were unleashed on the rest of Europe.

Those

of us paying attention may have easily lost count of the terror

atrocities carried out across Europe by Islamic fanatics. Charlie

Hebdo, Bataclan, the Bastille Day truck attack in Nice, the Brussels

airport, the Berlin Christmas Market were only the most recent and

spectacular. For years, individuals have been stabbed, had their

heads cut off, throats cut, been blown up, machine-gunned. Take a

look at this

comprehensive list going

back to 2001. You may be astonished. In that light, it’s pretty

hard to keep waving the “diversity” banner, and I sense that

Europe has had enough of it. One big question is whether the new

European right-wing leaders will actually move as far as mass

deportations. I rather think they will.

The

UK “Brexit” vote was surprise all right. (I hit a white-tailed

deer on the Maine Turnpike at 70mph that June morning, uccchhh,

and lived to tell about it.) Now there’s a fair chance that

Parliament will find a way to wiggle out of Brexit. Noises are also

emanating out of Brussels to the effect that the EU could loosen up

some of their rules — e.g. the Schengen Agreement — to induce

Britain to stay in the EU. But there are so many other fissures and

fragilities in that system that the Brexit may not matter anymore.

The European banking system is melting down and there is absolutely

no way to rescue it on the macro EU scale. Italy was heading for a

banking crackup before Christmas. Deutsche Bank has been whirling

around the drain for a couple of years. When the US markets and banks

shudder in 2017, Europe will get the vapors. Hence, I’ll forecast

breakup of the EU by this time next year.

We’ve

come to the pass where “all that is solid melts into air,” in the

poetic phrase of old Karl Marx. Marx was referring to the “specter”

of communism that loomed over burgeoning industrial society of the

mid-19th century,

and indeed it turned into quite a world struggle through the century

that followed. But now communism is down for the count and we begin

to see what is truly melting into air: Modernity itself, this

colossal, hulking, grinding, machine of destruction that threatens

the global eco-system, and all its sub-systems including the human

realms of money and politics.

The

idea that Modernity itself might go down is inconceivable to those in

thrall to the Religion of Progress, which declares that the world

(and life in it) only gets better and better every year. This would

appear demonstrably untrue, just in the visible damage to the

landscape and the living things that struggle to dwell there. The

most obvious problem with Modernity has been human population

overshoot. The truth is, we’re not going to do a darn thing about

it.

There won’t be any policy or protocol, despite the good

intentions of the groups inveighing against it. It will just go on…

until it can’t, to paraphrase the late Herb Stein. Of course,

people still have sex under conditions of hardship, so the population

may plateau for a while until we are well into the long emergency.

But the usual suspects of starvation, disease, and war are all still

out there, doing their thing, and will only ramp up their operations.

The

reason the Middle East and North Africa are melting down most

conspicuously is because they are geographically among the places

least well endowed for supporting the swollen populations they

acquired over the past two hundred years. Iraq, Syria, the whole

Arabian peninsula. Egypt, Libya, et. al. are all deserts artificially

supported by the perquisites of Modernity: cheap energy, fertilizers

made from that, irrigation, money derived from it, and

continuing life-support subsidies from even wealthier modern nations

outside the region. In recent years that life-support has flipped

into deadly violence imposed from both within and without, as

homegrown Sunni ad Shiite vie for supremacy and their puppeteers in

the First World rush in with bombers, rockets, and small arms to

“help.”

Iraq

and Libya were already goners in 2016. They’ll never be politically

stable again in the modern sense. Egypt is still headed down the

drain despite the grip of General al-Sisi and his army. In all these

places the “youth bulge” has no prospects for earning a living or

supporting a family. The young men, especially, put their energy into

Jihad, revolution, and civil war because there’s nothing else to

do. Making war may be thrilling, but it won’t lead to a better

future because those benefits of Modernity are running out and

there’s nothing to replace them.

Syria

is the current goner-du-jour. Whatever it ends up being, either under

Assad or someone else, it will not be stable the way it was. The USA

ended up arming and funding the Sunni Salafist “bad guys” there

because they opposed Shiite Iran and its regional proxy Hezbollah

plus Assad. Russia eventually came in on that side on the theory that

another failed state is not in the world’s interests. President

Obama blinked after he drew his infamous “line in the sand” years

ago and now America is too spooked to act directly. In fact, the

Russians and Assad have the best chance of restoring a semblance of

order, but America’s support for the “moderate” Salafists will

necessarily keep undermining that. In the meantime, all this activity

has sparked a demographic emergency as refugees flee the country for

Europe and elsewhere, creating greater tensions where they land.

Trump could stop the flow of US arms to our favored maniacs in Syria.

He may see the practical benefit of letting Russia be the policeman

on the beat there, and maybe he can sort out the underlying competing

interest between the Russian-sponsored gas pipeline proposed to cross

Syria and the American-sponsored one — a dynamic underlying all the

mayhem there — and make some kind of “deal.” Or maybe he’ll

just fuck it up even more.

The

situation will grow increasingly acute in Saudi Arabia, where

population growth outstrips the ability of oil production to pay for

it. Their old “elephant” oil fields are aging out and they know

quite well that they cannot depend on oil wealth many decades ahead.

The trouble is, they have no realistic replacement for it, despite

noises about creating other industries. The truth is, the country was

cursed by its oil. It grew its population too much too fast in one of

the most inhospitable corners of the globe, and it will take only a

modest decline in oil income to destabilize the place altogether. To

buffer that, Saudi leaders plan an IPO for shares in Saudi Aramaco —

which was originally composed of American and western oil companies

nationalized decades ago. That may get them a few hundred billion or

so in walking-around money that won’t last very long considering

that just about everybody in the nation is on the dole.

The

big news in that corner of the world last year was the collapse of

Yemen, which occupies a big slab on Saudi Arabia’s southern border.

That poor-ass country is the latest Middle East basket-case and Saudi

military operations there continue to date, using airplanes and

weapons supplied by Uncle Sam — just another case of feeding

Jihadist wrath.

Make

no mistake — as our Presidents like to say — all these countries

are heading back to the Middle Ages economically, maybe even further

beyond. Their culture is still basically medieval. The main point is

that Modernity inflated them and now Modernity is over and they’re

either going to pop or deflate. One wild card for now is what effect

climate change may have in ME/NA. If the trend is hotter, than that’s

not good news for a region so poorly watered and so hot that air

conditioning is mandatory for the pampered urban elites. Last one

out, please turn off the lights.

Then

there’s Turkey, for decades known as “the sick man of Europe.”

Now, of course, it can’t even get into Europe, the EU, that is, and

it’s probably too late to sweat that anyway. Back when it was

“sick” it was quiet at least. You barely heard a peep from the

fucker through the entire cold war and beyond. But now that the

countries on its border are breaking down, things have understandably

livened up in Turkey. It was, until World War One, the very seat of

the Islamic Caliphate, and it controlled much of the territory now

occupied by the nations creatively carved out of the Sykes-Picot

Agreement.

Turkey is still a power in the region, with a lot of

well-watered, habitable territory and a GDP half the size of Italy’s,

though shrinking. Its current president, Recep Tayyip Erdogan, has

shown twinges of megalomania in recent years, no doubt in fear of the

radical Islam epidemic so close at hand.

Lately, Kurdish extremists

have been planting bombs around the country, too. Turkey has a lot to

be paranoid about and Erdogan wants to change the constitution so he

can act the strongman without a wimpy, pain-in-the-ass parliament

weighing him down. He endured a coup last summer and came out of with

consolidated power. But he’s capable of making another bonehead

move like shooting down a Russian jet (2015). Meanwhile, Turkey’s

currency is collapsing. The population is over 80 million. In the

event of serious political upheaval, how many of them will try to

flee to Europe?

Russia?

It’s apparently stable. We hear no end of complaints about “Putin

the Thug,” but in this time of altered reality and disinformation

fog, it’s honestly impossible to tell what the fuck the score is.

Has he bumped off some journalists? So they say. But, not to get to

baroque about it, consider the impressive trail of dead bodies said

to be left in the wake of Bill and Hillary.

That story was so toxic

that Google squashed searches for it during the election campaign.

Putin seems to me, at worst, a competent and capable Czar, in a

country that likes to be ruled by them. That’s their prerogative.

He’s hugely popular, anyway, and it’s one of the unsung miracles

of recent times that Russia transitioned out of the fiasco of

communism into a pretty much normal modern society, with shopping,

movies, tourism travel, and everything. The Russian people may look

back at these decades as a golden age. They’ve been punished by

Western sanctions for a few years now, but it has prompted them to

promote their own version of a SWIFT Code for international banking

transactions, and their own counterpart to the EU, the Eurasian

Customs Union, and to manufacture some products of their own (import

replacement).

Personally,

I think the meme of “Russian aggression” is not born out by

actual recent geopolitical reality. They are castigated constantly

for wanting to march back into the Baltic States, Ukraine, and other

former Soviet territories. Ukraine was made a basket case with direct

American assistance. (Remember Deputy Secretary of State Victoria

Nuland: “Fuck the EU!”) Ukraine was rendered an instant failed

state. As far as I could tell, the last thing Russia wanted was to

take on Ukraine as an economic dependent.

Same for the Baltic States.

They need to subsidize these places like they need a hole in the

head. Russia’s 2015 annexation of the Crimea was a special case,

since it had been part of Russia one way or another for most of the

past 200 years, except for the period after Khrushchev gifted it to

his homeboys in Ukraine around 1957. Anyway, the Crimea was the site

of Russia’s only warm-water naval ports. They’d rented it from

Ukraine before the US pranged the country. The Crimean inhabitants

voted to join Russia (why do we assume that was not sincere?).

Finally,

as renowned Russologist Stephen Cohen has said, wouldn’t it make

sense for the US and Russia to drop all this antagonism nonsense and

make common cause against the real threat of our time: Islamic Jihad?

How many Westerners has Russia killed or harmed the past twenty years

compared to the forces of Jihad? The tensions in Syria are admittedly

complex, but why are we making them worse while Russia attempts to

stabilize the joint? Perhaps The Donald can start there….

As

I write, Mr. Putin just announced that his country would not take any

reciprocal action against American diplomats in retribution for Mr.

Obama’s fugue of punishments meted out last week for the

still-unproven “Russia Hacks Election” story. Personally, I’m

content to wait three weeks and see if relations improve after Mr.

Obama departs the Oval Office.

Finally,

there’s China. I’m among those who believe China is running the

most farkakta banking

system on God’s green earth. We should not be surprised if it

implodes in 2017, and does so pretty badly, in a way that might shake

the foundations of the entire banking system. On that note, I confess

that I have run out of forecast mojo for the year, and anyway this

bulletin in long enough. If you’ve gotten this far, I commend and

admire you hugely for your remarkable patience. Have a happy 2017

everybody, and don’t let our Trumpadelic president get you down.

No comments:

Post a Comment

Note: only a member of this blog may post a comment.