Ore

Ships Seen Taken Out of Service If Earnings Drop Further

20

December, 2014

A

deeper slump in earnings for ships that carry most of the world’s

coal and ore cargoes would force owners to take vessels out of

service, according to shipbroker RS Platou Markets AS.

Average

daily earnings for Capesize ships fell to $3,735 today, the lowest in

more than two years, according to data from the Baltic Exchange in

London. Rates will probably remain low next year, according to Herman

Hildan, shipping analyst at Platou.

“At

the moment, they’re barely covering their operating costs,”

Hildan said by phone today from Oslo. “It doesn’t make sense for

owners to participate in fixing vessels” if rates fall further.

Signs

of slowing growth in China, the world’s largest importer of thermal

coal and iron ore, have caused a collapse in Capesize rates of about

90 percent this year. China’s economy will expand by 7 percent next

year, the slowest growth in a quarter century, according to economist

forecasts in a Bloomberg survey. Customs data showed a slump in ore

imports in November.

Hildan’s

own estimates show Capesize vessels are currently earning $6,900 a

day on average. Shippers would begin taking their vessels out of

service when the daily rate falls below $5,000, he said.

The

rate for the vessels, which can carry as much as 160,000 metric tons

of iron ore, has averaged $13,923 in 2014, according to Baltic

Exchange data. Analysts were expecting daily earnings of $18,500,

according the median of estimates gathered by Bloomberg in January.

“It

looks like the market is going to continue being a big

disappointment” in 2015, Hildan said.

Commodity

Prices Are Cliff-Diving Due To The Fracturing Monetary Supernova -

The Case Of Iron Ore

30

December, 2014

Crude

oil is not the only commodity that is crashing. Iron

ore is on a similar trajectory and for a common reason. Namely,

the two-decade-long economic boom fueled by the money printing

rampage of the world’s central banks is beginning to cool rapidly.

What the old-time Austrians called “malinvestment” and what

Warren Buffet once referred to as the “naked swimmers”

exposed by a receding tide is now becoming all too apparent.

This

cooling phase is graphically evident in the cliff-diving

movement of most industrial commodities. But

it is important to recognize that these are not indicative of

some timeless and repetitive cycle—–or an example merely of the

old adage that high prices are their own best cure.

Instead, today’s

plunging commodity prices represent something new under the sun. That

is, they are the product of a fracturing monetary supernova that was

a unique and never before experienced aberration caused by the

1990s rise, and then the subsequent lunatic expansion after

the 2008 crisis, of a cancerous regime of Keynesian central

banking.

Stated

differently, the worldwide

economic and industrial boom since the early 1990s was not indicative

of sublime human progress or the break-out of a newly

energetic market capitalism on a global basis. Instead,

the approximate $50 trillion gain in the reported global

GDP over the past two decades was an unhealthy and unsustainable

economic deformation financed by a vast outpouring of fiat

credit and false prices in the capital markets.

For

that reason, the

radical swings in commodity prices during the last two decades mark

the path of a central bank generated macro-economic bubble, not

merely the unique local supply and demand factors which pertain

to crude oil, copper, iron ore, or the rest. Accordingly,

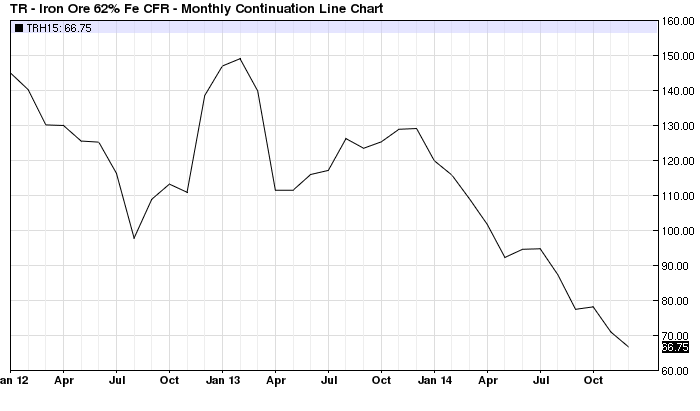

the chart below which shows that iron ore prices have plunged from

$150 per ton in early 2013 to about $65 per ton at present only

captures the tail end of the cycle.

What

really happened is that the central bank instigated global

macro-economic bubble ripped commodity pricing cycles out of their

historical moorings, resulting in a one time eruption of price levels

that had no relationship to sustainable supply and demand factors in

the mines and petroleum patch. What materialized, instead, was an

unprecedented one-time mismatch of commodity production

and use that caused pricing abnormalities of gargantuan proportions.

Thus,

the true free market benchmark for iron ore is the pre-1994

price of about $20-25 per ton. This represented the

long-time equilibrium between advancing mining technology and

diminishing ore grades available to steel mills in the DM economies.

But

as shown below, after Mr. Deng institutionalized export

mercantilism and printing press prosperity in the form of China’s

red capitalism in the early 1990s, iron ore prices broke orbit and

soared to $100 per ton in the second half of the decade and

then went parabolic from there. After peaking at $140 per ton on

the eve of the financial crisis,China’s mad cap “infrastructure”

stimulus boom after 2008 drove the price to a peak of $180 per ton in

2011-2012. To wit, iron ore prices peaked at nearly 9X their historic

range.

The

crucial point is that there was nothing normal, sustainable or

economic about the $180 per ton peak. It was a pure deformation of

central bank credit expansion and the accompanying false pricing of

debt and other forms of long-term capital.

Needless

to say, the same thing is true of copper. Its historical benchmarks

were in the 60 cents to 100 cents per pound range. Yet after 1994,

the global bubble—again led by the enormous credit explosion

and currency exchange rate suppression in China and its BRIC

satellites—carried the price to $4 per pound in the eve of

the financial crisis, and then to nearly $5 during the peak of

China’s post-crisis credit explosion.

Indeed,

in the case of copper, not only was the cycle driven by unsustainable

construction demand; it was also powered by dodgy forms of

financial engineering that turned copper inventories into financing

collateral that was sometimes re-hypothecated many times over.

The

exact same considerations apply most especially to crude oil.

China’s GDP grew from $1 trillion to $9 trillion during the 13

years after the turn of the century. Growth of such enormous

proportions is not remotely possible in an honest economy based on

productivity, savings, investment and sound money. Likewise,

China’s call on the global oil supply system—-which soared by

4X from 3 million bbls/day to nearly 12 million—–is also a

drastic aberration; it is a product of runaway credit creation that

financed false “demand”.

And

that was only the beginning of the aberration. The

China engine pulled additional false petroleum demand into the world

market equation due to the boom among its suppliers—such as

Brazil, Canada and Australia for raw materials and South Korea

and Taiwan for components and parts. Output levels and

petroleum consumption in Germany and the US were also goosed by

China’s voracious demand for German capital goods and

Caterpillar’s heavy machinery, for example.

Accordingly,

the crude oil price path shown below reflects the same

global monetary supernova. The

$20 price in place during the 1990s was no higher in inflation

adjusted terms than it had been one century earlier when the

mighty Spindletop gusher was discovered in East Texas in 1901. By

contrast, the 5X eruption to north of $100 per barrel during

this century represents the impact of fiat credit and false

capital market prices deforming the entire warp and woof of the

global economy.

Self-evidently,

we are now in the cliff-diving phase, but unlike the bounce after the

September 2008 financial crisis, there will be no rebound this time

around. That is owing to two reasons.

First,

most of the world is at “peak debt”. That

is, the ratio of total credit market debt to current national income

ranges between 350% and 500% in every major economy; and that is the

limit of what can be serviced even at today’s aberrantly low

interest rates.

As

Milton Friedman famously observed, markets are ultimately not fooled

by the money illusion. In this case, the illusion is that today’s

sub-economic interest rates will last forever and that debt carrying

capacity has been elevated accordingly.

Not

true. Short-term interest rates may be temporarily and

artificially pegged at the zero bound by central bankers,

but at the end of the day debt carrying capacity is tethered by real

economics and normalized costs of money and debt.

Accordingly,

the central banks are now pushing on a string. The credit

channel of monetary transmission is over and done. The only

remaining effect of the residual level of money printing still

underway is that ZIRP enables carry trade gamblers to drive

financial asset prices ever higher, thereby setting up another

thundering collapse of the financial bubbles being generated for the

third time this century by the world’s central banks.

The

second reason for no commodity price rebound is

the monumental overhang of the malinvestments which have been

made, especially since the 2008 crisis. That is obviously what is now

pummeling the petroleum sector.

The

huge expansion of high cost crude oil capacity—–in the shale

patch, tar sands and deep off-shore—-was due to the aberrationally

high price of oil and the inordinately cheap cost of capital

which were generated during the last two decades by the global

central banks. The above price chart for the WTI marker price of

crude, for example, is what explains the eruption of shale oil

production from 1 million bbls/day prior to the financial crisis to

more than 4 million at present., not an alleged technological miracle

called “fracking”.

However,

the iron ore capacity expansion story is no less cogent. On the eve

of the financial crisis, the Big Three miners—-Vale, BHP and

Rio—had already doubled their mining capacity from 250 million tons

annually at the turn of the century, to 195 million tons per quarter

or 780 million tons annually.

But

when prices soared to $180/ton in 2012, investment levels were

drastically scaled-up even further. Currently, the Big Three have

combined capacity of more than 1.1 billion tons annually that is not

only in the investment pipeline, but is actually so far advanced that

completion makes more sense than abandonment.

Accordingly, not

withstanding the massive over-supply already in the market, several

hundred million more tons will compound the surplus and drive prices

even closer to the out-of-pocket cash cost of production in

the years immediately ahead.

The

above depicted capacity expansion is a quintessential reflection of

the manner in which false prices in the capital markets drive

excessive and wasteful investment, and cause the crash following the

credit driven boom to be all the more destructive. So

the cliff-diving price action here is not just another commodity

cycle, but instead is a proxy for the fracturing global

credit bubble, led by China department.

During

the course of its mad scramble to become the world’s export

factory and then its greatest infrastructure construction site,

China’s expansion of domestic credit broke every historical record

and has ultimately landed in the zone of pure financial madness. To

wit, during the 14 years since the turn of the century China’s

total debt outstanding–including its vast, opaque, wild west shadow

banking system—soared from $1 trillion to $25 trillion, and from 1X

GDP to upwards of 3X.

But

these “leverage ratios” are actually far more dangerous and

unstable than the pure numbers suggest because the

denominator—national income or GDP—-has been erected on an

unsustainable frenzy of fixed asset investment. Accordingly,

China’s so-called GDP of $9 trillion contains a huge component of

one-time spending that will disappear in the years ahead, but which

will leave behind enormous economic waste

and monumental over-investment that will result

in sub-economic returns and write-offs for years to come. Stated

differently, China’s true total debt ratio is much higher

than 3X currently reported due to the unsustainable bloat in its

reported national income.

Nearly

every year since 2008, in fact, fixed asset investment in public

infrastructure, housing and domestic industry has amounted to nearly

50% of GDP. But

that’s not just a case of extreme of growth enthusiasm, as the

Wall Street bulls would have you believe. It’s actually

indicative of an economy of 1.3 billion people who have gone mad

digging, building, borrowing and speculating.

Nowhere

is this more evident than in China’s vastly overbuilt steel

industry, where capacity has soared from about 100 million tons in

1995 to upwards of 1.2 billion tons today. Again,

this 12X growth in less than two decades is not just red capitalism

getting rambunctious; its actually an economically cancerous

deformation that will eventually dislocate the entire global

economy. Stated differently, the 1 billion ton growth of

China’s steel industry since 1995 represents 2X the entire capacity

of the global steel industry at the time; 7X the size of Japan’s

then world champion steel industry; and 10X the then size of the

US industry.

Already,

the evidence of a thundering break-down of China’s steel industry

is gathering momentum. Capacity

utilization has fallen from 95% in 2001 to 75% last year, and will

eventually plunge toward 60%, resulting in upwards of a half

billion tons of excess capacity. Likewise, even the manipulated

and massaged financial results from China big steel companies have

begin to sharply deteriorate. Profits have dropped from $80-100

billion RMB annually to 20 billion in 2013, and are now in the

red; and the reported aggregate leverage ratio of the industry has

soared to in excess of 70%.

But

these are just mild intimations of what is coming. The hidden truth

of the matter is that China would be lucky to have even 500 million

tons of annual “sell-through” demand for steel to be used in

production of cars, appliances, industrial machinery and for normal

replacement cycles of long-lived capital assets like office towers,

ships, shopping malls, highways, airports and rails. Stated

differently, upwards of 50% of the 800 million tons of steel

produced by China in 2013 likely went into one-time demand from

the frenzy in infrastructure spending.

Indeed,

the deformations are so extreme that on the margin China’s steel

industry has been chasing its own tail like some stumbling, fevered

dragon. Thus,

demand for plate steel to build dry bulk carriers has soared, but the

underlying demand for new bulk carrier capacity was, ironically,

driven by bloated demand for the iron ore needed to make the steel to

build China’s empty apartments and office towers

and unused airports, highways and rails.

In

short, when the credit and building frenzy stops, China will be

drowning in excess steel capacity and will try to export its way out—

flooding the world with cheap steel. A

trade crisis will soon ensue, and we will shortly have the kind of

globalized import quota system that was imposed on Japan in the early

1980s. Needless to say, the latter may stabilize steel prices at

levels far below current quotes, but it will also mean a drastic

cutback in global steel production and iron ore demand.

And

that gets to the core component of the deformation arising

from central bank fueled credit expansion and the drastic worldwide

repression of interest rates and cost of capital. The 12X expansion

of China’s steel industry was accompanied by an even more fantastic

expansion of iron ore production, processing, transportation, port

and ocean shipping capacity.

On

the one hand, capacity could not grow at the breakneck speed of

China’s initial ramp in steel production—so prices soared.

And again, not just in the range of traditional cyclical

amplitudes. As indicated above, prices rose from $20 per ton in

the early 1990s to $180 per ton by 2012—meaning that vast windfall

rents were earned on the difference between low cash costs on

existing or recently constructed iron ore capacity and the soaring

prices in spot and contract markets.

The

reality of truly obscene current profits and the propaganda about

endless growth in the miracle of red capitalism, combined with the

cheap debt available in global capital markets, resulted in an

explosion of iron ore mining capacity like the world has never

before witnessed in any mineral industry.

Stated

differently, the Big Three miners would never have expanded their

capacity from 250 million tons to 1.1 billion tons in an honest free

market. Nor would they have posted such egregious financial trends as

have occurred over the past decade. To wit, even as the global iron

ore (and also copper) boom gather steam in the run-up to the

financial crisis, the three miners spent $55 billion on CapEx during

the four years ending in 2007.

By

contrast, during the four most recent years they spent 3.2X more or

$175 billion. Not surprisingly, the residue on their balance sheets

is unmistakable. Their combined debt went from about $12 billion in

2004 to more than $90 billion at present.

But

now, prices will be driven down to the lowest marginal cost of

supply, meaning that Big Three EBITDA will violently collapse,

causing leverage ratios to soar and new CapEx to be drastically

downsized. In turn, Caterpillar’s order book will take a giant hit,

and so will its supply chain running all the way back to Peoria.

So

the collapse of the mother of all commodity bubbles is

virtually baked into the cake. As

one industry CEO recently acknowledged, his company’s truly

variable, cash cost of production is about $20 per ton and he

will not hesitate to keep producing for positive variable profit.

That means iron ore prices will also plunge far below the current $66

per ton quote now extant in the market.

In

short, when the classical Austrians talked about “malinvestment”

the pending disasters in the global steel and iron ore industries

(and also mining equipment and other supplier industries) are what

they had in mind. Except none of them could have imagined the

fevered and irrational magnitudes of the deformations that have

resulted from the actions of the mad money printers who now run

the world’s central banks.

No comments:

Post a Comment

Note: only a member of this blog may post a comment.